Weekly Tech+Bio #81: AI Agents at the Cancer Conference

AI-pharma deals track toward a 12x increase in five years, Life Biosciences takes reprogramming to Phase 1, and Jeito closes Europe's largest independent biopharma fund

AACR 2026 dropped its abstract data and the AI footprint is now large enough to read structurally. We dig into what ~1,100 AI-related abstracts reveal about where the field is actually moving. Elsewhere: a few deals and pipeline moves worth tracking, a €1B European fund close, and the ongoing question of who captures value when pharma and AI companies partner.

Also, if you're at Drug Discovery Chemistry in San Diego this week, our board advisor Andrew Lozoniuk is there and happy to chat!

Hi! This is BiopharmaTrend’s weekly newsletter, Where Tech Meets Bio, where we explore technologies, breakthroughs, and cutting-edge companies.

If this newsletter is in your inbox, it’s because you subscribed, or someone thought you might enjoy it. In either case, you can subscribe directly by clicking this button:

🤖 AI x Bio

(AI applications in drug discovery, biotech, and healthcare)

Agents at AACR 2026

At the American Association for Cancer Research annual meeting this year, out of ~9,600 accepted abstracts roughly 1,100 (1 in 8) are AI-related, according to Miraei AI.

Within that: ~160 reference LLMs, generative AI, or agentic systems; ~140 involve multimodal approaches; ~225 cite clinical validation or deployment language. The Miraei team’s read is that AI in oncology is shifting from isolated proof-of-concept models to embedded operational systems.

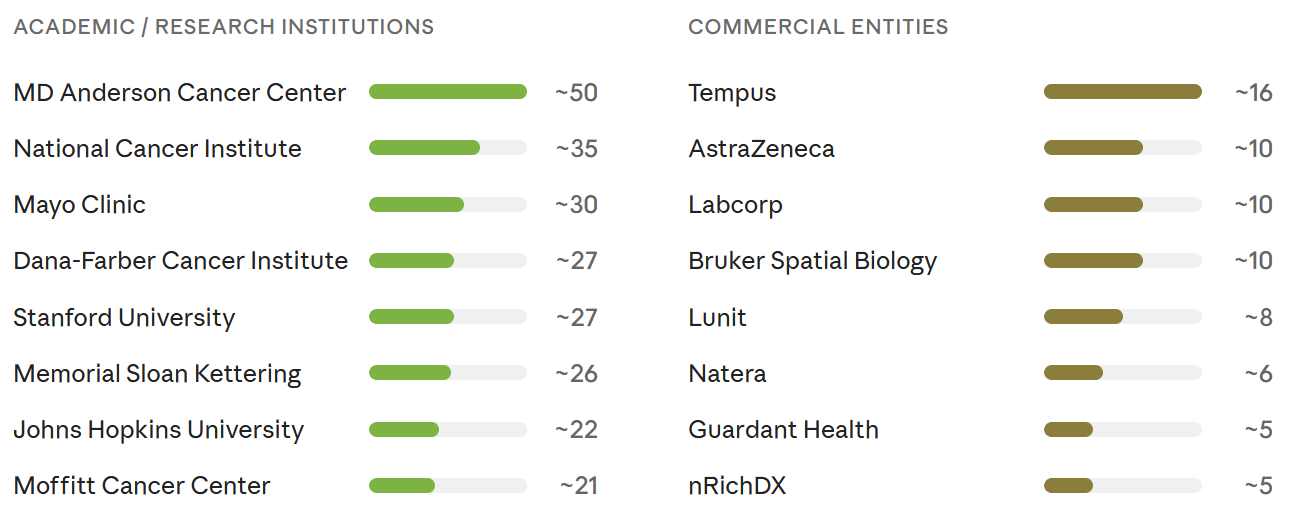

The leaderboard of AI-related abstract affiliations at AACR 2026, split by academic institutions and commercial entities:

AACR will host a dedicated “Agentic AI in Cancer” session: MD Anderson will debut “Charles,” a self-critical agentic drug discovery analyst built around traceability and hallucination mitigation. MSK will show an MCP-enabled AI agent in its genomics platform automating multimodal analysis at petabyte scale. AstraZeneca (the most-represented biopharma in the AI corpus with ~10 abstracts) will present an agentic system for RNA-seq pipeline automation. (AstraZeneca also acquired Modella AI earlier this year, whose Judith agent automates pathology image analysis workflows.)

Foundation models were still a distinct thread. Bioptimus delivered three abstracts including two late-breakers—H-optimus-1 for computational histopathology and M-Optimus-1, a multimodal model unifying H&E imaging, bulk and single-cell RNA-seq, and spatial transcriptomics. A UCSD–Lunit collaboration will present a foundation model of cancer genotype predicting therapeutic response.

Around 225 abstracts use language suggesting clinical validation or deployment, not just modeling accuracy on retrospective data. A separate “LLMs in the Clinic” session (~30 abstracts) will focus on infrastructure problems: trial matching, EHR extraction, pathology report abstraction, patient message triage. A University of New Mexico study reported cancer patients preferred ChatGPT-generated responses to physician-authored ones in a blinded comparison.

This tracks with what we covered in our February deep dive on AI in oncology. The pattern across ~1,100 abstracts is the same shift we described there: from standalone models to infrastructure. Agentic systems managing multi-step workflows, LLMs doing clinical plumbing, foundation models trained at institutional scale. Commercial actors (Tempus, Labcorp, Lunit, Natera, BMS) are showing operational work; the startup layer (Bioptimus, Data4Cure, Keiji AI, EXoPERT) is landing late-breaking slots.

AI in the pipeline

A few recent moves worth noting across clinical trials, pharma infrastructure, and AI-designed therapeutics.

🔹 Massive Bio published a prospective study in ESMO Real World Data and Digital Oncology with 3,804 cancer patients, 17,000+ oncologist-confirmed trial matches, 4x faster matching (120-to-30 min per patient), outperforming zero-shot GPT-4 and GPT-4o.

🔹 CRO Fortrea released an AI suite for clinical workflow automation, part of CEO Anshul Thakral’s turnaround strategy since taking over in June 2025.

🔹 Tempus expanded its collaboration with Gilead with enterprise-wide access to Tempus’s Lens platform for oncology R&D, continuing the pattern of large pharma outsourcing data infrastructure to specialized AI/RWE companies.

🔹 Astellas exercised its option to license a Dyno Therapeutics AAV capsid for skeletal muscle gene delivery, following Roche’s CNS capsid license in January 2025 — making Dyno the first company to license AI-designed capsids for both CNS and muscle ($15M fee plus milestones and royalties).

💰 Money Flows

(Funding rounds, IPOs, and M&A for startups and smaller companies)

Daniel Strasser, Executive Director and Therapeutic Area Biomarker Head at Novartis, posted a tracking that puts the pace of AI-pharma deals in perspective.

Between 2021 and 2024, top pharma signed 2–4 AI deals per year. In 2025: 15. At Q1 2026 pace, the year is tracking toward ~24 — a 12x increase in five years.

Combined potential deal value across 34 tracked partnerships exceeds $78B. All top-10 pharma like Lilly, Novartis, Roche, Sanofi, AstraZeneca, J&J, Novo Nordisk, Takeda are in with billion-dollar-scale commitments.

NVIDIA alone ($4.4T) is worth more than all top-10 pharma combined ($3.5T), and the AI-pharma pure-plays signing these deals collectively sit around $23B.

Strasser's question is—which side captures the value?

Cell reprogramming in the clinic

Longevity raise—Life Biosciences (co-founded by David Sinclair) closed an $80M Series D for the Phase 1 trial of ER-100—reportedly the first partial epigenetic reprogramming therapy to receive FDA IND clearance. ER-100 uses AAV2 vectors encoding three Yamanaka factors and an oral small-molecule switch, targeting retinal ganglion cells in optic neuropathies.

Q1 2026 was strong for longevity biotech overall ($3.7B across 49 deals, 56% YoY). Competitors remain largely preclinical:

Altos Labs (~$3B, stealthy)

Retro Biosciences ($1B+ Series A, clinic-stage autophagy)

NewLimit ($130M Series B, liver)

Life Bio’s differentiator is clinical specificity, though the sector still has to prove it can produce credible aging biomarkers alongside disease-specific efficacy.

Europe’s largest independent biopharma raise?

Jeito Capital closed Fund II at over €1B (~$1.2B). The fund targets 15-to-20 clinical-stage investments at up to €150M each, addressing a funding tier where European options have historically been thin.Fund I (€534M, 2021) exits include Eyebiotech (Merck, $1.3B) and Hi-Bio (Biogen, $1.15B).

For context: between 2015 and mid-2025, EU biotech startups attracted €25B in venture capital versus €219B in the US, and 66 of the 67 EU companies that went public over the past six years listed on foreign exchanges.

🔹 A digital therapeutic for negative symptoms of schizophrenia—Click Therapeutics got $50M Series D from Boehringer Ingelheim plus full commercial rights for CT-155. Phase III CONVOKE met its primary endpoint (p=0.0003, Cohen’s d = –0.36). Click already has two authorized digital therapeutics (migraine, major depressive disorder) and 63 patents.

🔹 The OpenAI Foundation announced $100M+ in initial grants for Alzheimer's research across five tracks: causal mapping (Arc Institute), AI-assisted drug design (Institute for Protein Design + Mass General Brigham), open datasets (EvE Bio), biomarkers (UCSF), and off-patent treatment testing (Harvard). David Baker's IPD team says they've already engineered molecules that engage and degrade Alzheimer's-relevant targets using AI protein design models. The off-patent track is notable: lithium orotate and the shingles vaccine both have suggestive evidence but no private-sector incentive to fund proper trials. More grants expected through 2026.

🏛️ Bioeconomy & Society

(News on centers, regulatory updates, and broader biotech ecosystem developments)

🔹 Neuropacs received De Novo classification from the FDA for a diffusion MRI–based AI diagnostic aid that helps differentiate atypical Parkinsonian syndromes (MSAp, PSP) from Parkinson’s disease. The classification establishes a new regulatory category “Parkinsonian syndrome diagnostic aid,” and is the first device in it. The tool draws on 15+ years of research and a prospective multicenter study across 21 centers (Parkinson Study Group, published in JAMA Neurology). Neuropacs recently closed a $1M seed round.

⚙️ Other Tech

(Innovations across quantum computing, BCIs, gene editing, and more)

🔹 Can it deliver? Quantum computing is drawing pharma bets. Amgen has worked with Quantinuum since ~2018 and invested in its $300M round in 2023—building competence now for utility that’s 5–10 years out. Novo Holdings is assembling a portfolio (Sparrow Quantum, Phasecraft) and says it’s “confident tangible quantum advantage for defined applications will be achieved before 2030.” VC in quantum hit $3.8B in 2025. Merck KGaA’s Thomas Ehmer offered the counterpoint: the field is “always three years away,” and whether the killer app justifies advance competence-building remains open.

🔹 Miltenyi Biomedicine’s CAR-T drove three autoimmune diseases into simultaneous remission in a single patient—AIHA, antiphospholipid syndrome, and immune thrombocytopenia, all B-cell–driven and previously treatment-resistant. Eleven months out remission holds. Kyverna Therapeutics is likely first to an autoimmune CAR-T approval (stiff-person syndrome, FDA submission expected H1 2026).

Cover: Antique celestial map illustration with mythological constellations and star charts from an early 19th century astronomy book, published in London in 1822. iStock

Read also:

Three Big Ideas in Aging Research That Could Shift the Therapeutic Landscape