New-Modality Drugs Behind Today’s Big Headlines

How advanced therapeutics are solving “undruggable” biology and creating industry’s most valuable assets

A lot has been happening lately across biopharma spanning massive deals and landmark approvals. Madrigal Pharmaceuticals has signed a $4.4B agreement with China’s Ribo Life Science to co-develop six preclinical siRNA therapies targeting metabolic dysfunction–associated steatohepatitis (MASH). Earlier, during the JPM week, AbbVie announced a $5.6B deal with RemeGen for a PD-1xVEGF bispecific antibody aimed at treating solid tumors. Meanwhile, Eli Lilly acquired CAR-T developer Orna for $2.4B, and the FDA approved the first oral GLP-1 therapy for weight loss, developed by Novo Nordisk.

At first glance, these headlines span different companies and medical areas. But they share a common thread: each centers on advanced therapeutic modalities (ATMs)—a new generation of medicines that go beyond the limits of conventional drugs.

According to BCG, eight of the top ten best-selling biopharma products in 2025 are new-modality drugs, and the global pipeline value for these therapies has reached $197B. ATMs are becoming a more established part of the industry and are noticeably contributing to its growth.

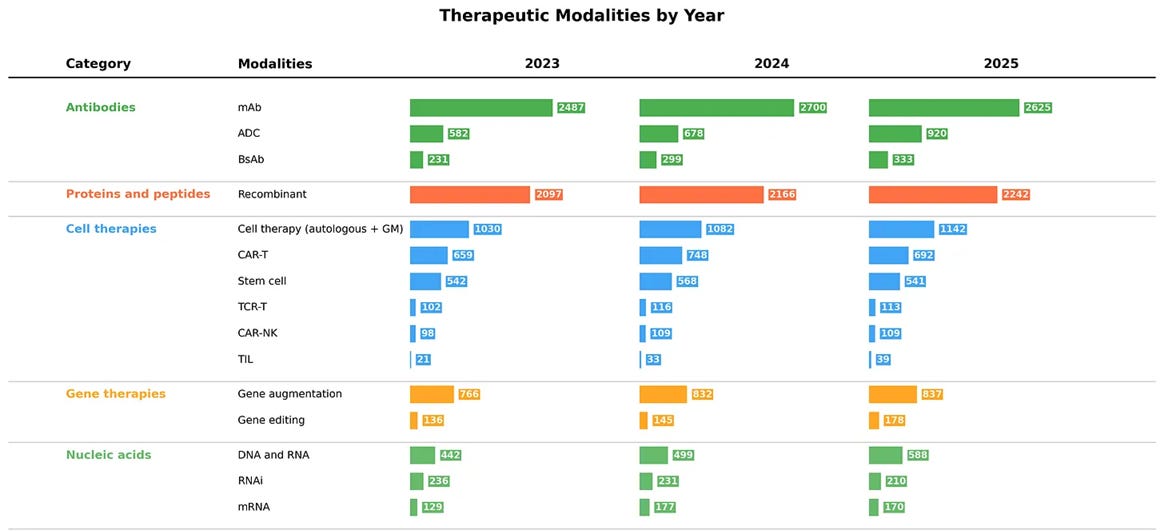

In this issue: Reject Tradition, Embrace Modernity — A World In Between — Antibodies — Proteins and Peptides — Cell Therapies — Gene Therapies — Nucleic Acids — Targeted Protein Degraders — Lookahead